Why and how is every e-invoice mandate different?

Understanding the nuances behind the differences in e-invoice mandate involves delving into both straightforward and complex factors. While the technical “how” is easier to explain, the “why” encompasses broader economic, political, and historical contexts. Often, the why and how go together, making it challenging to draw a clear distinction.

Why do e-invoice mandates differ?

Despite the potential benefits of a unified global e-invoicing model, significant differences exist due to historical contexts, economic strategies, political factors, and stakeholder interests.

Historical practices shape current e-invoicing regulations and standards. The evolution of each country’s tax and financial systems over time leads to unique features in their e-invoicing requirements. National economic policies and strategies also play a role. Different economic goals, such as enhancing competitiveness or increasing tax revenues, shape the e-invoice mandates. The trend is that many countries today focus on stringent e-invoicing to minimize tax evasion and increase compliance.

Political decisions significantly influence the design and implementation of e-invoicing systems. The political landscape and issues of sovereignty often lead to varied mandates. For example, while the EU provides general guidelines, individual member states retain the autonomy to design specific mandates, reflecting political preferences.

Finally, the interests of various stakeholders, including businesses, tax authorities, and policymakers, lead to varying requirements and features in e-invoicing mandates. Large multinational companies might push for industry-specific requirements or more standardized systems, while local businesses may prefer simpler, less costly solutions. These diverse objectives and contexts ensure that e-invoice mandates remain varied across different regions.

How do e-invoice mandates differ?

Let’s take a closer look at how e-invoicing and mandates differ with some examples. Especially in the past, the level of technological advancement and digital infrastructure available in a country has played a role. For example, Nordic countries have advanced e-invoicing networks due to their robust infrastructure, supported by an advanced invoice automation market that boosts e-invoice ratios. This has led to a situation where a “mandate” has not really been necessary (even though there have been those on the B2G side). Business interests have been a large enough driver initially.

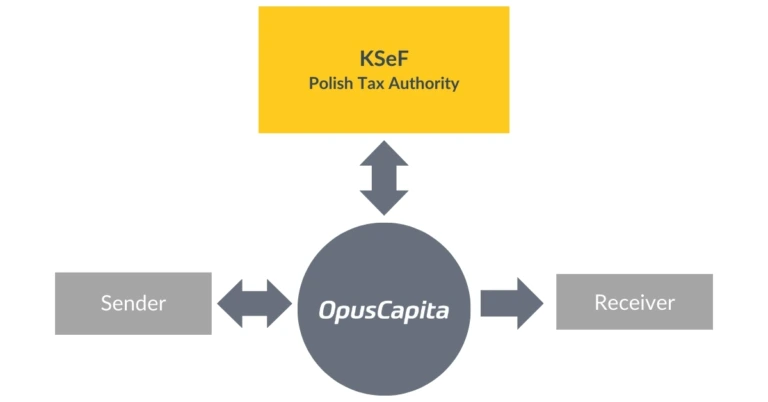

Today, each country typically has distinct laws and regulations governing taxation and financial reporting. These frameworks dictate specific e-invoicing requirements, such as mandatory information, invoice format, and submission methods. For instance, Italy’s FatturaPA system requires invoices to be in a specific XML format, ensuring consistency and compliance with national standards. In contrast, Germany will most likely accept various EN-compliant formats when the e-invoicing mandate in Germany takes effect in January 2025 onwards, similar to many other countries. In Poland, all invoices are considered issued only in the national KSeF platform after a specific registration process, while in the majority of European countries, invoices are issued when generated in sellers’ systems. In some countries, PDFs via email are not considered e-invoices, even though they are still very widely used, e.g., in North America.

Compliance objectives have greatly impacted the mandates. A very typical objective in many countries is to minimize the VAT gap. This has led to very strict and often extremely complex models that are highly governed. For example, service providers often need to have local accreditation, like in Italy. Some countries have also targeted fraud prevention, such as Brazil’s Nota Fiscal, which requires detailed tax codes to prevent tax evasion. Others, like Singapore, focus on streamlining business processes and reducing administrative burdens through simplified e-invoicing standards.

Typically, the need for e-invoicing systems to integrate seamlessly with national tax authorities, banking systems, and business software is a requirement. Variations in existing systems necessitate different e-invoicing solutions. In Mexico, for instance, e-invoices must be submitted in real-time to the SAT for validation before being sent to the buyer, integrating tightly with national tax systems. This is a burden naturally to companies operating in multiple different countries.

In many models today, tax reporting integrated into e-invoicing processes plays a significant, if not driving, role. Various implementations exist, with many countries having their own nuances. Attempts to harmonize these processes also exist, such as ViDA, which is greatly impacting the European models currently being planned and launched.

Modelling different approaches (by billentis)

To ease the understanding of the different models, it is convenient to categorize and classify them into a few primary ones. For example, the consulting company billentis has categorized e-invoice models into four principal baskets in their recent e-invoicing and tax compliance report “Watch the tornado”:

Real-time reporting model

In the real-time reporting model, taxpayers must quickly report invoices to the tax administration shortly after invoice issuance. This involves a central processing platform established by the tax authority and accessed via accredited software. Taxpayers must submit invoice data within 24-72 hours post-issuance, allowing flexibility in the data submitted. This model recognizes various invoicing practices, such as electronic and human-readable formats like PDFs. Challenges include the need for separate reporting systems and the inclusion of additional data, increasing costs. This model is used in countries like Hungary and South Korea.

Clearance model

The clearance model requires invoices to be checked for tax compliance and approved before being sent to the recipient. This can occur pre-clearance or post-clearance and may involve single (simplex) or dual (duplex) party reporting. A central platform verifies tax compliance before forwarding the invoice. Challenges include operational burdens, lack of standardization, and limited automation. This model is used in countries like Chile and Mexico.

Centralized exchange model

In the centralized exchange model, a central platform facilitates invoice exchange and tax reporting for both B2G and B2B transactions. Sellers submit invoices to the platform, which validates format, tax compliance, and business rules before sending them to the buyer. Challenges include reliance on a single platform, system integration modifications, and potential disruption to trade cycle automation. Countries using this model include Italy, Serbia, and Turkey.

Decentralized CTC and exchange model (5-corner model)

The decentralized CTC and exchange model involves certified service providers handling data validation and exchange. Businesses interact with service providers through a single interface, and a selected portion of the invoice is reported to the central tax authority platform. Advantages include customization for different tax requirements, SME-friendly services, and reduced risk of a single point of failure. This model is designed to meet both fiscal and business automation needs. Unfortunately, the complexity level is high. France is implementing this model.

Key takeaway?

In summary, the differences in e-invoice mandate are driven by unique regulatory frameworks, technological infrastructures, compliance objectives, integration needs, and legal and cultural differences. Historical contexts, economic strategies, political factors, and stakeholder interests further complicate the landscape, making each mandate distinct.

As a business, you must adhere to local legislation, and this includes complying with e-invoicing mandates. There are no exceptions.

Kamil Cichocki, Product Manager, E-invoice Compliance

The challenge lies in the fact that many of these mandates are newly implemented and evolving. Not only are you affected, but so are all your business partners, necessitating a collective adaptation. Adding to the complexity, these mandates will continue to evolve, with significant changes expected as various tax reporting models are integrated with e-invoicing.

The key takeaway is to start preparing now. Build a strategy to tackle e-invoice compliance immediately. Delaying compliance could lead to penalties and disrupt your business operations. Remember the benefits: enhanced and potentially fully automated financial processes will save you money and improve efficiency in the medium to long term.

Read more about the e-invoice mandate in Poland.

Read more about the e-invoice mandate in Germany.

About the author

Kamil is an expert in e-invoicing compliance working in Product Management and building solutions in the e-invoicing domain.

Name of the game: Excellence in e-invoicing compliance

Uncover the critical elements and game-changing strategies in the constantly shifting e-invoicing compliance landscape – and most importantly, learn how to master it. Get also updates on the latest changes in Germany, Poland, Belgium, Estonia, and Denmark.

Free webinar on September 4th, 2024, at 9 AM CET