Poland’s e-invoice mandate: A (rocky) path to digital transformation

Poland is on a transformative journey to reshape the landscape of how companies exchange invoices. Poland’s e-invoice mandate will be enforced in alignment with EU directives, this mandate expects businesses to issue and receive invoices electronically through the National E-Invoicing System (KSeF). While the initiative promises increased efficiency, reduced administrative burdens, and a crackdown on tax fraud, its implementation has encountered delays, leaving businesses in suspense regarding its enforcement date.

What is Poland’s e-invoicing mandate?

At the core, Poland’s e-invoice mandate is an idea of a classical Central Tax Control (CTC) model, necessitating real-time registration of invoices through the government portal.

While CTC models are prevalent in regions like Latin America and APAC, they have remained relatively rare in Europe. Italy, as the first European country, rolled out a full B2B mandate after running a B2G mandate in the beginning, inspiring later countries like France, Germany, and Belgium to follow their models.

Despite their tax-focused design, CTC models offer one significant silver lining for businesses by facilitating a complete shift to e-invoices, thereby enhancing operational efficiency and automation.

Status of Poland’s e-invoicing mandate today

Although this model’s use has been voluntary since 2022, the adoption has been low. Many use cases have required clarifications and still some details are open. Originally Poland’s e-invoice mandate was supposed to take effect on the 1st of January 2024, but it was postponed to the 1st of July 2024.

Ministry of Finance has recently informed that the mandate will be delayed until 2026. Companies with a turnover of more than PLN 200 million yearly will be impacted 1st of February and the rest 1st of April 2026. Ministry of Finance has also stated that changes to already published processes will be announced later, so a variety of details are still open.

We are still expecting detailed information from the government about how to move forward – this impacts directly to customer projects

Mariusz Jastrząb

How is it going to impact on businesses?

Once effective, the mandate casts a wide net, impacting all B2B invoicing activities in Poland. Any entity obliged to pay VAT, indicated by possessing a Numer Identyfikacji Podatkowej (NIP) number, falls under its purview. B2C transactions, tickets, and invoices are excluded under EU special procedures such as OSS and IOSS.

The fate of Business-to-Government (B2G) transactions is under evaluation by the Ministry of Finance. While the existing PEF platform facilitates B2G invoicing via Peppol, plans to integrate or “merge” it with KSeF have encountered delays.

Changes to operational processes

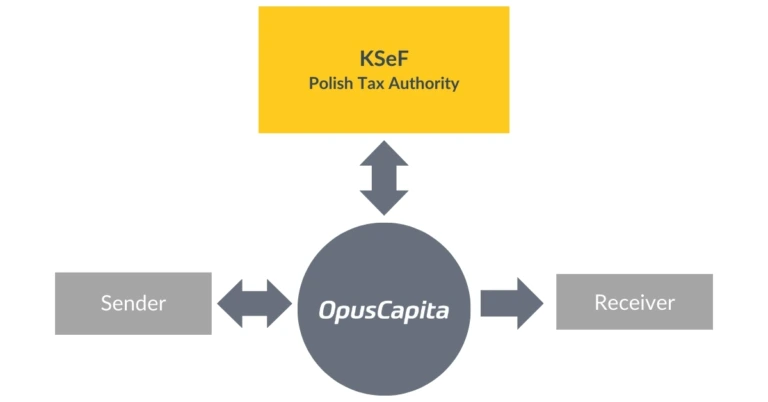

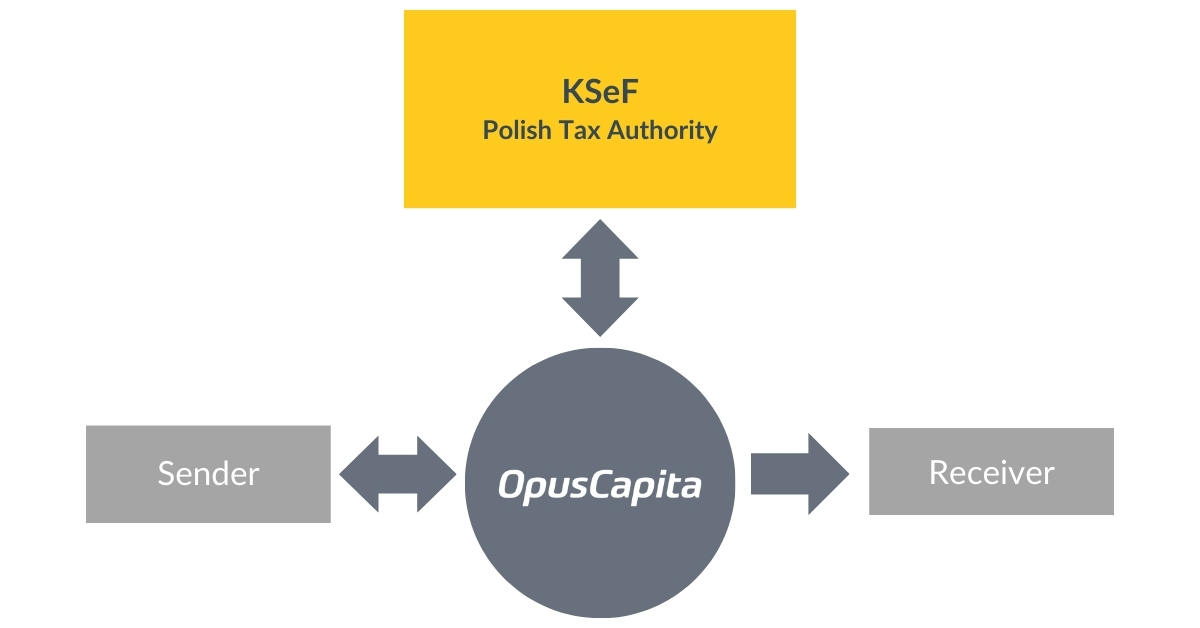

The KSeF platform serves as an intermediary between invoice senders and receivers. Invoices must be submitted to KSeF for registration, resulting in the issuance of a unique KSeF identifier and an Urzędowe Poświadczeniu Odbioru (UPO) document. While KSeF handles registration, it doesn’t regulate invoice delivery, allowing various delivery channels post-registration.

More detailed view:

Submission to KSeF: Upon generating an invoice, businesses must submit the invoice data to the KSeF platform for registration. This submission triggers the issuance of a unique KSeF identifier and UPO document, essential for legal compliance.

Registration and issuance: The registration process within KSeF marks the official issuance of the invoice. Interestingly, this registration step also serves as the delivery mechanism, even though KSeF itself doesn’t provide traditional delivery channels like operator networks or Peppol access.

Delivery channels: While KSeF manages the registration aspect, it doesn’t dictate the invoice delivery method. The mandate assumes that receivers will receive invoices via KSEF. For non-domestic invoices existing channels to send and receive invoices will remain.

Receiver end: On the recipient end, invoices registered in KSeF are considered legally valid. This means that any invoice received via the KSeF platform bears the unique identifier. holds legal weight. Businesses can integrate their systems to automatically process invoices received through KSeF, ensuring compliance with minimal manual intervention.

Archiving: KSeF also serves as an invoice archive, storing invoices and related documents for a period of 10 years. While this centralized archiving solution simplifies compliance with local regulations, businesses may need to adapt their internal archiving processes to align with country-specific requirements.

Next steps?

Ensure that necessary projects are scoped and commenced. Regardless of the new timelines, there’s no need to risk business continuity. By taking proactive steps, such as:

Assessment: Evaluate your current invoicing processes and systems to identify gaps and areas for improvement in compliance with the e-invoice mandate. Assess also the non-domestic invoice sending and receiving process.

Engagement: Engage with relevant stakeholders, including finance, IT, and legal teams, to align on the impact of Poland’s e-invoice mandate and develop a comprehensive implementation strategy. Consider engaging also with your business partners, suppliers, and customers.

Technology readiness: Assess your existing technology infrastructure and capabilities to determine if any upgrades or investments are necessary to support e-invoicing requirements.

Vendor evaluation: Conduct thorough evaluations of vendors to ensure compatibility, reliability, and compliance with regulatory standards. Remember to consider also cross-border invoicing and vendor capabilities to support that.

Training and awareness: Provide training and awareness sessions to employees to familiarize them with the new processes and tools associated with e-invoicing.

Testing and piloting: Conduct testing and piloting of e-invoicing processes to identify any potential issues or challenges before full-scale implementation. Piloting is possible since platform usage is voluntary.

Legal compliance: Stay informed about updates and changes in regulatory requirements related to e-invoicing and ensure ongoing compliance with all relevant laws and regulations.

Advice to companies impacted by the mandate: Start preparing today

Mariusz Jastrząb

By proactively addressing these aspects, companies can mitigate risks, ensure a smooth transition to e-invoicing, and maintain business continuity regardless of any shifts in timelines associated with the mandate.

Conclusion

Despite challenges, Poland’s e-invoice mandate heralds a significant stride toward digital modernization in invoicing practices. While compliance demands careful planning and investment in technology, the benefits – enhanced efficiency, reduced fraud risks, and improved transparency – are significant.

Navigating this mandate requires collaboration among stakeholders, ensuring a seamless transition and reaping the rewards of digital transformation. As Poland progresses towards a fully digital invoicing ecosystem, businesses embracing this change stand poised for a more efficient and sustainable future.